Understanding SIF categories India 2026 starts with one investor — Ramesh, a textile business owner in Surat. He is 46 years old, earns well, and has accumulated ₹10 lakh sitting in a savings account earning almost nothing. He is not new to investing — he has mutual funds running, a few FDs, and some LIC policies from years ago.

If you are new to structured investing, our Investment Guide for Gujarat Business Owners is a good starting point.

But this ₹10 lakh feels different. He does not want another ordinary SIP. He has seen enough market cycles to want something smarter — something that does not just go up and down with the Sensex. He walks into his relationship manager’s office and says three words that sum up what millions of Indian HNI investors feel today: “I want more.”

More than a regular mutual fund. Less than the ₹50 lakh PMS minimum he cannot justify yet. Something in between — institutional-grade strategy, mutual fund convenience, without the ultra-HNI ticket size.

That product exists now. It is called a Specialised Investment Fund — SIF. And understanding what is actually inside each category is the difference between Ramesh making a smart decision and simply chasing a new label.

“Every week I meet investors who have outgrown plain vanilla mutual funds but are not ready for PMS. SIF was built exactly for them. But like any new product, the label is simple — the DNA inside is complex. My job as a distributor is to decode that DNA in simple language so my clients can make a confident decision — not a confused one.”

— Paresh Chaudhary, Founder, Shree Radha Financial Services, Surat

What is a SIF — In One Line

SEBI created the Specialised Investment Fund in 2024 to fill a gap that has existed in India’s investment landscape for years. Think of it this way:

| Product | Minimum Investment | Strategy Flexibility | Regulation |

|---|---|---|---|

| Regular Mutual Fund | ₹500 SIP | Long only — strict style box | SEBI — MF regulations |

| SIF — Specialised Investment Fund | ₹10 lakh minimum | Long-short, derivatives, REIT/InvIT — institutional grade | SEBI — MF regulations |

| PMS | ₹50 lakh minimum | High flexibility — direct stock portfolio | SEBI — PMS regulations |

| AIF | ₹1 crore minimum | Maximum flexibility — institutional and alternatives | SEBI — AIF regulations |

One line: A SIF gives you PMS-style strategy inside a mutual fund wrapper — at a ₹10 lakh entry point.

The Indian SIF market has already scaled past ₹13,182 crore in total AUM as of May 2026 — in less than a year since launch. That is not distributor momentum alone. That is serious capital moving into a new category with genuine conviction.

But SIF is not one product. It is a family of three very different strategies — each with its own DNA, its own risk profile, and its own ideal investor. Decoding each one is what this article is about.

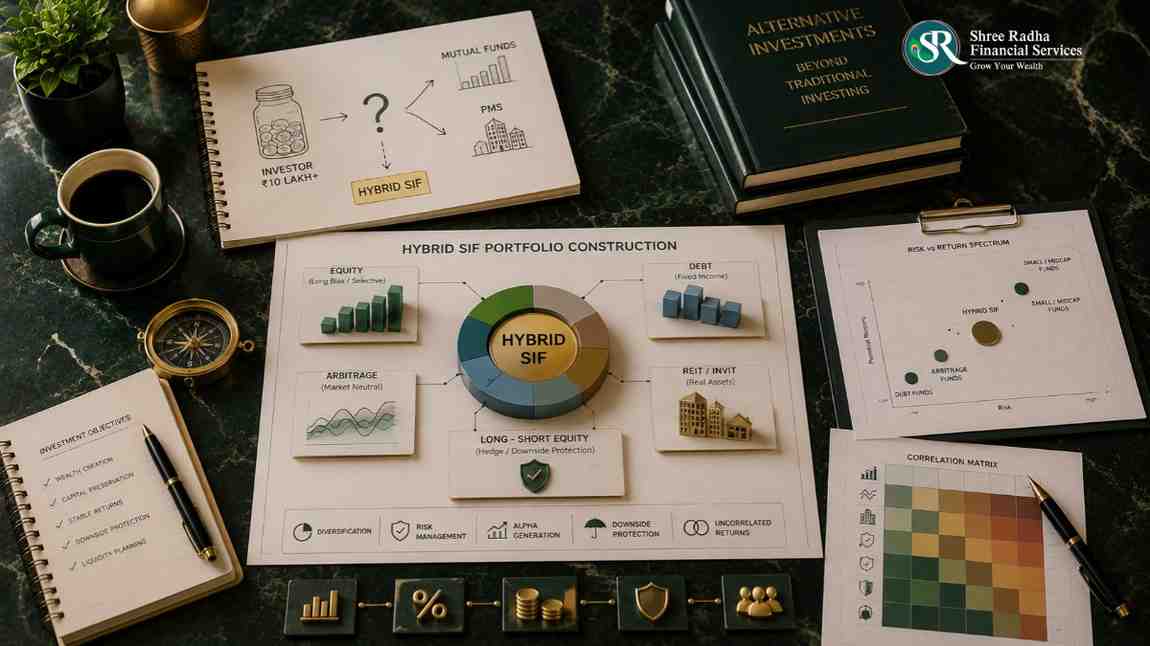

SIF Categories India 2026 — Hybrid SIF The All-Weather Portfolio DNA

Meet Sunil. He is a 48-year-old chemical industry business owner from Surat — the kind of investor who has done everything right. Mutual funds running. FDs in place. A commercial property generating rental income. His portfolio is solid.

But one question has been bothering him for two years: “When the market crashed in March — why did my balanced advantage fund still fall 14%?”

He is not looking for magic. He just wants something that earns meaningfully in good times and does not fall sharply in bad ones. His FD gives 7.2% but feels inadequate. His equity funds feel volatile. He wants something intelligent — sitting right between the two.

That is exactly the problem a Hybrid SIF was designed to solve.

What is Actually Inside a Hybrid SIF — The Real DNA

Here is the most important thing about Hybrid SIF that almost no article explains clearly: the better Hybrid SIFs carry almost zero directional equity risk. They are not equity funds with a hedge. They are income-first strategies that use arbitrage as their foundation — with selective equity and derivative overlays on top.

Look at Edelweiss Altiva — the largest Hybrid SIF in India, which has crossed ₹5,000 crore in AUM. Here is its actual portfolio construction from the May 2026 factsheet:

| Strategy Layer | Altiva Allocation (May 2026) | What It Does |

|---|---|---|

| Cash-Future Arbitrage & Covered Call | 47% | Captures near-risk-free spread between cash and futures — market neutral, low volatility income |

| Fixed Income | 53% | High quality bonds — AAA/SOV 69%, AA+ 11%, AA 20% — blended YTM of 8.39% |

| REITs and InvITs | 4% | Office parks and infrastructure trusts — steady predictable yield from physical assets |

| Other Derivative Strategies | 11% | Straddle, strangle, put-call parity — capitalising on market volatility without directional bets |

| Special Situations | 0.4% | IPOs, open offers, buybacks, merger arbitrage — selective event-driven opportunities |

The total crosses 100% because of leverage within the arbitrage structure — this is normal and expected in such strategies.

The key insight: Altiva holds almost no net long equity position. The 45% showing as “Equity and Equity Related” in the portfolio is almost entirely arbitrage pairs — every long stock position is paired with a matching short futures position, making it effectively market-neutral. This is fundamentally different from a balanced advantage fund that actually owns stocks and hopes they go up.

The Proof — What Happened in March 2026

In March 2026, the Nifty 50 fell sharply by 11.31% — one of the steepest single-month corrections in recent memory. Sunil’s balanced advantage fund fell 14%. What did Altiva do?

Altiva fell just 1.54%.

Since inception in October 2025, the Nifty has delivered a negative annualised return of approximately -14%. Altiva has delivered +10.99% annualised in the same period — with significantly lower volatility. That is not a marketing claim. That is the factsheet number from May 2026.

This is the Hybrid SIF answer to Sunil’s question. Not magic. Just a structurally different strategy that does not need the market to go up to earn.

Hybrid SIF Taxation — What You Need to Know

Because Hybrid SIFs like Altiva hold less than 65% in directional equity, they are taxed differently from equity mutual funds:

| Investor Type | If Held Under 12 Months | If Held Over 12 Months (LTCG) | Compared to FD Interest |

|---|---|---|---|

| Resident Indian — 30% slab (HNI) | Taxed at 30%+ slab | 12.5% LTCG | FD interest taxed at 30%+ every year — significant post-tax advantage in LTCG |

| Resident Indian — 20% slab | Taxed at 20% slab | 12.5% LTCG | Meaningful post-tax advantage over FD |

| Quant QSIF Hybrid — special rule | At income slab | 12.5% — but only after 24 months | Plan your exit timeline carefully — 24 months not 12 |

For Sunil — a business owner in the 30% tax bracket — the difference between paying 30% on FD interest every year and 12.5% LTCG on a Hybrid SIF after 12 months is substantial. On ₹10 lakh of returns over 3 years, that tax difference alone can mean ₹1.75 lakh more staying in his pocket.

This is not just a return story. It is a tax-efficiency story for resident Indian HNIs.

According to AMFI India, SIF operates under the mutual fund regulatory framework.

Important note for NRI investors: Tax treatment for NRIs investing in SIF depends on applicable DTAA between India and your country of residence and your individual tax profile. Please consult a qualified cross-border tax advisor before investing. The figures above apply to resident Indian investors only.

Check before investing: Altiva currently qualifies for 12-month LTCG. Quant QSIF requires 24 months. Always verify the holding period requirement from the fund’s SID — it varies by AMC.

Ex-Top 100 Long-Short SIF — The Smallcap and Midcap DNA Nobody Else Has

Now meet Vikram. He is a 50-year-old diamond merchant from Surat with a strong equity portfolio. He already has large-cap funds, a midcap fund, and some smallcap exposure. He is not new to market volatility — he has lived through 2008, 2020, and every correction in between.

Vikram’s frustration is specific: “My midcap fund went up 40% in 2023. Then it gave back 22% in 2024. I want the upside of midcap and smallcap — but I am tired of watching it fall just as fast as it rose.”

Regular midcap and smallcap mutual funds cannot solve Vikram’s problem. They are long-only vehicles — they can only buy stocks and hold cash. When the market falls, they fall with it. There is nothing the fund manager can do except wait.

The Ex-Top 100 SIF changes this completely.

Three Things an Ex-Top 100 SIF Can Do That No Regular Fund Can

1. Short up to 25% of the portfolio using derivatives

When the fund manager believes specific midcap or smallcap stocks are overvalued — or the broader market is turning — they can take short derivative positions. A short position profits when the stock price falls. In a market correction, these shorts generate gains that partially offset losses in long positions. No regular mutual fund in India has this tool.

2. No style-box restriction

A regular midcap mutual fund must invest at least 65% in the 101st to 250th ranked companies by market cap. It cannot go below that — even if the fund manager sees a brilliant opportunity in the 300th or 500th ranked company. An Ex-Top 100 SIF simply says: anything outside the top 100 is fair game. The fund manager can freely move between midcap, smallcap, and microcap based on where the opportunity is — without triggering any style-drift penalty.

3. Concentrated, high-conviction portfolio

Regular funds managing thousands of crores struggle to exit illiquid smallcap positions quickly when redemption pressure hits. Because SIFs use structured redemption frameworks — not daily open-ended exits — the fund manager can build a genuinely concentrated, high-conviction portfolio of 20 to 30 companies without worrying about sudden mass redemptions forcing them to sell at bad prices.

The HNI Question — Why Not Just Buy a Smallcap Mutual Fund?

Vikram asked this directly. Here is the honest answer:

A regular smallcap mutual fund gives you broad market exposure with daily liquidity. That is valuable. But it cannot short overvalued stocks, cannot move freely across the midcap-smallcap-microcap spectrum, and cannot build the concentrated conviction positions that generate true alpha over a market cycle.

If Vikram is investing ₹10 lakh or more, has a 3 to 5 year horizon, and wants genuine structural alpha from the ex-top-100 universe — not just index-like returns in a fancy wrapper — the Ex-Top 100 SIF offers something structurally different. The ₹10 lakh minimum is not a barrier. It is a filter — ensuring only committed, informed capital enters.

Currently ICICI Prudential’s iSIF Equity Ex-Top 100 Long-Short Fund and 360 ONE’s DynaSIF Equity are among the prominent launches in this category. More AMCs are expected to follow through 2026.

Equity Long-Short SIF — The Bear Market DNA Question

And now the question that every HNI investor asks when they first hear about Long-Short SIFs: “Does it actually protect me when the market crashes — or is the shorting just decorative?”

This is the most honest and important question in the entire SIF conversation. Let us answer it directly.

What a Long-Short Equity SIF Actually Does

An Equity Long-Short SIF targets the broader equity universe — often without the ex-top-100 restriction — and uses a combination of long positions in stocks the manager believes will rise, and short derivative positions in stocks or indices the manager believes will fall.

The goal is not just to reduce losses in a falling market. The goal is to generate positive returns across all market cycles — what the industry calls an absolute return strategy.

The Equity Long-Short SIF AUM has surged past ₹1,622 crore total in mid-2026 — the fastest growing subcategory within SIF — as capital allocators specifically seek absolute alpha outside expensive large-cap names.

The Honest Answer on Bear Market Protection

Here is what most SIF marketing material will not tell you clearly — and what a good distributor must say.

Most Equity Long-Short SIFs are net-long in normal market conditions. They may have 70 to 80% in long positions and 20 to 25% in short derivative hedges. In a mild correction, the shorts cushion the fall meaningfully. In a severe bear market — a 2008 or March 2020 style crash — the shorts provide partial protection, not complete insulation.

By late March 2026, all five live equity-oriented SIF strategies on AMFI’s NAV page were below their issue prices. This is important context for new investors — SIFs are not capital-protected products. They are sophisticated active strategies with a longer performance horizon. Judge them over a full market cycle — 3 to 5 years — not over 6 months.

The real value of the long-short mechanism is not eliminating drawdowns. It is generating better risk-adjusted returns over a full cycle — capturing more of the upside while losing less on the downside — compared to a plain vanilla equity fund.

Which SIF Is Your Story — A Simple Decision Table

Ramesh is back in his RM’s office. He has heard the DNA of all three SIF categories. Now comes the question every investor asks: “Which one is for me?”

| Your Profile | What You Want | SIF That Fits | Hold Period |

|---|---|---|---|

| Sunil — Surat chemical business owner, tired of FD returns, wants better tax efficiency and stable growth with low volatility | Steady income — not equity volatility, significantly better than FD after tax over 12 months | Hybrid SIF | 2 to 3 years minimum |

| Vikram — Experienced investor, already has large-cap and midcap funds, wants true alpha from ex-top-100 universe | Genuine structural edge in midcap/smallcap — not just another midcap fund | Ex-Top 100 Long-Short SIF | 5 years minimum — full market cycle |

| Arjun — NRI professional, experienced equity investor, wants absolute return strategy across market cycles,NRI investors can also read our Middle East NRI Investment Guide for the complete India investment roadmap. | Positive returns across market conditions — not just in bull markets — managed by institutional team | Equity Long-Short SIF | 5 years minimum — full market cycle |

| Priya — Working professional, ₹10 lakh is her 6-month emergency fund, might need it anytime | Liquidity above all — this ₹10 lakh must be accessible | No SIF — liquid funds or FD | Not applicable |

The last row is as important as the first three. SIF is not for every ₹10 lakh. It is for ₹10 lakh that is genuinely investable — money you will not need for at least 2 to 3 years, sitting above your emergency fund, beyond your existing liquid financial safety net.

The Liquidity Warning — Read This Before You Invest

For a broader view of how SIF compares with PMS, read our SIF vs PMS comparison guide.This is the section that no SIF brochure highlights prominently. A responsible distributor must say it clearly.

Several SIFs do not offer daily redemption. Some use interval structures — redemption windows that open weekly, fortnightly, or monthly. Some have exit loads that apply for 1 to 2 years after entry. The exact liquidity terms vary by AMC and scheme.

High-profile financial advisors across India’s wealth community are actively posting warnings about this on LinkedIn: do not treat SIF capital as part of your liquid emergency layer. This is not money you can redeem in 24 hours during a family emergency, a business cash crunch, or an unexpected medical expense.

Before committing ₹10 lakh to any SIF:

- Read the Scheme Information Document — specifically the redemption and liquidity section

- Confirm whether the fund has daily NAV and open redemption, or interval windows

- Ensure this ₹10 lakh is genuinely surplus — not touching your emergency fund, your children’s education fund, or your short-term business working capital

- Ask your distributor to model the exit load impact if you need to exit early

SIF is a long-term commitment instrument. Enter it only with long-term money.

Who Has Launched What — The SIF Landscape in 2026

| AMC | SIF Category | Fund Name |

|---|---|---|

| ICICI Prudential | Ex-Top 100 / Hybrid | iSIF Equity Ex-Top 100 Long-Short Fund / iSIF Hybrid Fund |

| Tata Mutual Fund | Hybrid Long-Short | Titanium Hybrid Long-Short Fund |

| Edelweiss | Hybrid Long-Short | Altiva SIF — crossed ₹5,000 crore AUM — largest Hybrid SIF in India |

| Quant Mutual Fund | Hybrid / Equity | QSIF Hybrid Long-Short Fund / QSIF Equity Fund |

| 360 ONE Asset | Multi-Asset / Equity | DynaSIF AAF / DynaSIF Equity |

| Bandhan Mutual Fund | Equity / Hybrid | Arudha Equity SIF / Arudha Hybrid SIF |

| SBI Mutual Fund | Hybrid Long-Short | Magnum SIF Hybrid Long-Short Fund |

More AMCs are launching SIF strategies through 2026. The category is young — fund track records are short. Choose based on AMC credibility, fund manager experience, strategy clarity, and liquidity terms — not NFO marketing alone.

Frequently Asked Questions — SIF Investing in India 2026

I already have midcap and smallcap mutual funds. Why would I add an Ex-Top 100 SIF?

Your existing midcap and smallcap funds are long-only — they can only buy stocks. In a correction, they fall with the market. An Ex-Top 100 SIF can short overvalued midcap stocks using derivatives — potentially cushioning the fall and generating alpha that your regular funds structurally cannot. It is not a replacement. It is a different tool for the same universe — with more degrees of freedom for the fund manager.

Can NRIs invest in SIF in India?

Yes. Unless specifically restricted in the Scheme Information Document, SIFs follow standard mutual fund practices for NRI investment — including from the USA and Canada. Investment is made through an NRE or NRO account. Tax treatment follows Indian mutual fund rules. Confirm with the specific AMC and your distributor before investing, as individual fund restrictions may apply.

Is SIF safe? What is the risk compared to a regular mutual fund?

SIF carries higher complexity risk than a regular mutual fund — it uses derivatives, short positions, and concentrated portfolios. This means it can underperform in the short term even when designed well. It is not capital-protected. Judge over a 3 to 5 year full market cycle. SIF is appropriate for investors who understand that higher sophistication does not mean lower risk — it means managed risk with a smarter toolkit.

What happens if I need to exit my SIF early?

This depends entirely on the specific fund’s SID. Some SIFs offer daily redemption with exit loads. Others use interval windows. Read the redemption terms before investing. Early exit during an interval window may not be possible — or may attract exit loads of 1% to 2%. Never invest money in SIF that you may need urgently.

I have ₹10 lakh. Should I put it all in one SIF or split across categories?

For a first-time SIF investor, a single well-chosen category based on your profile is cleaner than splitting across three categories you are still learning. Understand one SIF category deeply — invest with conviction — and expand as your familiarity grows. Spreading thinly across all three on day one often leads to confused expectations and premature exits.

Is the ₹10 lakh minimum per fund house or per fund?

The ₹10 lakh minimum is at the PAN level across all SIF strategies under one AMC — not per individual fund within that AMC. So if you invest ₹6 lakh in a Hybrid SIF and ₹4 lakh in an Ex-Top 100 SIF from the same AMC, you meet the minimum. Across different AMCs, the minimum applies separately per AMC.

Is SIF the Right Next Step for Your Portfolio?

Sunil left that conversation knowing exactly which SIF category matched his situation — and more importantly, which ones did not. That same clarity is available to every investor who reaches out.

Whether you are a Gujarat business owner with surplus capital, an NRI professional building India wealth from abroad, or a salaried investor ready to move beyond plain vanilla mutual funds — one honest conversation can bring your next step into sharp focus.

Grow Your Wealth — that is what we are here for.

📞 Call/WhatsApp: +91 98791 13255

📧 Email: shreeradha.services@gmail.com

🌐 Visit: www.srwealth.co.in

📍 Shop 33, Mira Nagar 2, Dindoli Road, Surat 394210

Paresh Chaudhary

Founder, Shree Radha Financial Services, Surat

AMFI Registered Mutual Fund & SIF Distributor — ARN: 268390

APMI Registered PMS Distributor — APRN05763

Investing since 2012 | BE Mechanical, SVNIT Surat | Ex-L&T (15+ Years)

Educational Disclaimer: This article is published by Shree Radha Financial Services — an AMFI Registered Mutual Fund & SIF Distributor (ARN: 268390) and APMI Registered PMS Distributor (APRN05763). All content is strictly for educational purposes only and does not constitute individualised investment advice. Mutual fund and SIF investments are subject to market risks — read all scheme-related documents carefully before investing. All AUM figures, NAV data, and fund performance mentioned are based on publicly available information as of mid-2026 and are subject to change. Tax treatment depends on individual investor profile and applicable laws — consult a qualified tax advisor before investing. Liquidity terms vary by scheme — refer to the Scheme Information Document of each fund before investing. Past performance is not indicative of future results.